The RBI has updated the Priority Sector Lending (PSL) norm in October 2022.

Priority sector lending (PSL) is aimed to provide institutional credit to those sectors and segments for whom it is difficult to get credit. According to priority sector norms, in general, most of the scheduled commercial banks have to give 40% of their loans (measured in terms of Adjusted Net Bank Credit or ANBC/ Credit Equivalent of Off-Balance Sheet Exposures (CEOBE)) to the identified priority sectors in accordance with the RBI regulations. There is separate limits for RRBs, Small Finance Banks and Urban Cooperative Banks. Local Area Banks also have to give PSL.

The regulations on PSL are modified periodically by setting limits for sectors and subsectors and other qualifications for the beneficiary groups. For example, several marginal changes were made on PSL norms in the context of the Covid pandemic. PSL is now extended to more sectors, including startups. Similarly, the limits for renewable energy, including solar power and compressed bio-gas plants, are increased.

The latest review was done by the RBI in October 2022. Changes were made in recent years, after the recommendations of the ‘Expert Committee on Micro, Small and Medium Enterprises (Chairman: Shri U.K. Sinha) and the ‘Internal Working Group to Review Agriculture Credit’ (Chairman: Shri M. K. Jain) apart from discussions with all stakeholders.

Several changes are made in PSL norms in recent years, and this includes new eligible categories: MSMEs, social infrastructure and renewable energy. A separate target for small and marginal farmers (8% for 2021, gradually to be increased to 10% by 2024), microenterprises (7.5%) and weaker sections (10% in 2021, to be increased 12% by 2024). The priority sector non-achievement is assessed on a quarterly average basis.

In April 2016, the RBI introduced Priority Sector Lending Certificates so that banks can trade the loan certificates given to the different sectors to meet their targets.

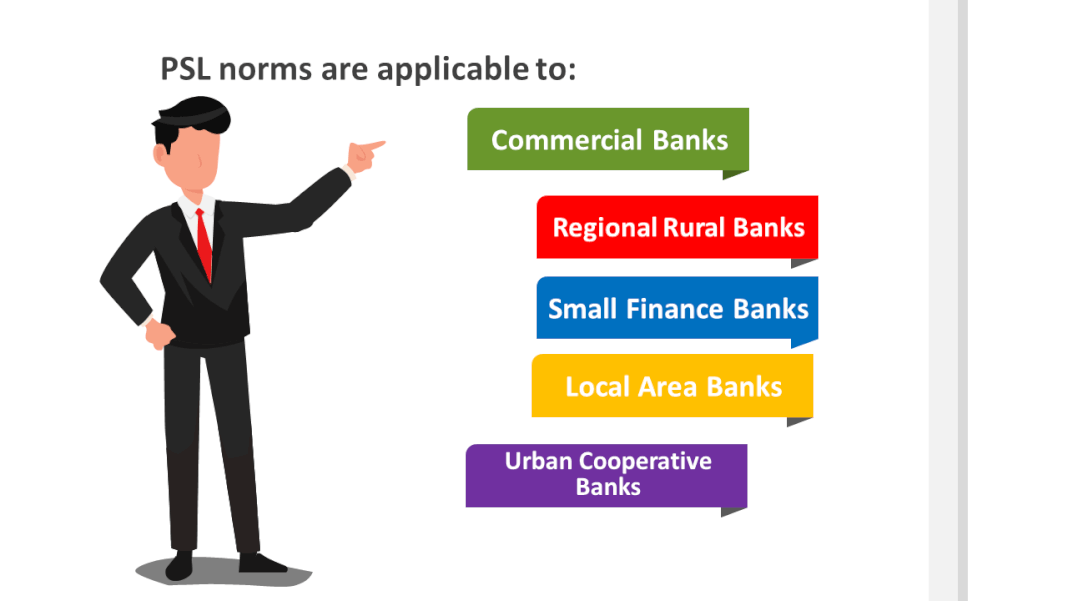

Banks that have to implement the PSL norms (Applicability of PSL norms):

- Commercial Banks [including Regional Rural Bank (RRB), Small Finance Bank (SFB), Local Area Bank] and

- Primary (Urban) Co-operative Bank (UCB) other than Salary Earners’ Bank.

UCBs have to achieve a PSL target of 75% by 2024 in a phased manner.

| Priority Sector Norm for various categories and banks in brief (UCBs separately given) | ||||

| Categories | Domestic commercial banks (excl. RRBs & SFBs) & foreign banks with 20 branches and above | Foreign banks with less than 20 branches | Regional Rural Banks | Small Finance Banks |

| Total Priority Sector | 40% | 40% | 75% | 75% |

| Agriculture | 18% | Not applicable | 18% | 18% |

| Micro Enterprises | 7.50% | Not applicable | 7.50% | 7.50% |

| Advances to Weaker Sections | 12% | Not applicable | 15% | 12% |

Loans here are expressed as a percentage of ANBC or CEOBE.

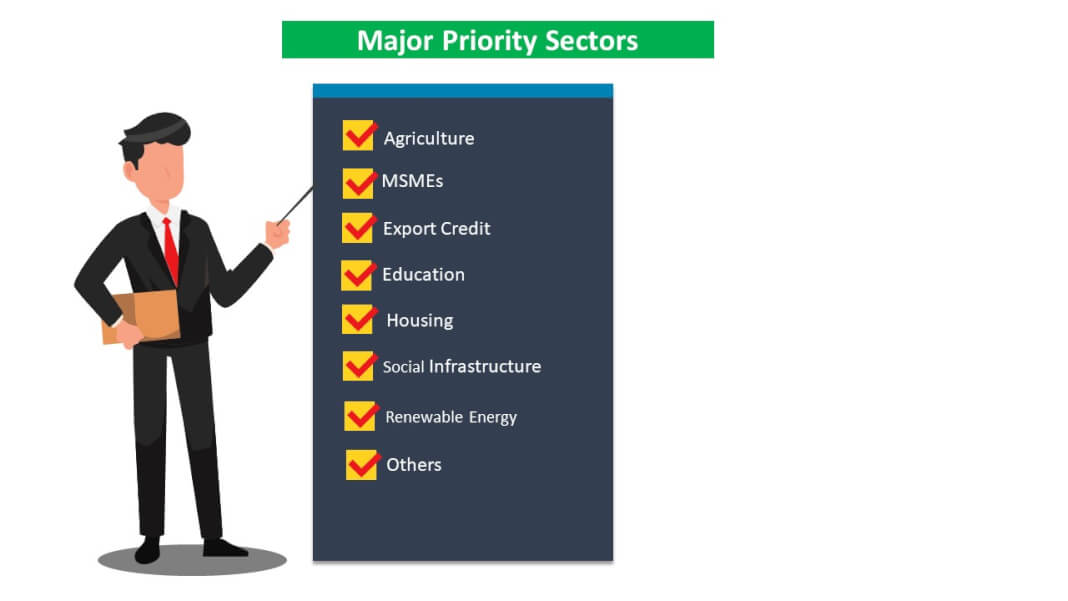

Important categories under priority sector

- Agriculture 18%: Agriculture sector will include Farm Credit (Agriculture and Allied Activities), lending for Agriculture Infrastructure and Ancillary Activities.

Within the 18 per cent target for agriculture, a target of 10 per cent of Adjusted Net Bank Credit (ANBC) is prescribed for Small and Marginal Farmers (with less than 2 hectares and 1 hectare respectively) by 2024 from 8% in 2021.

Credit to agriculture sector includes:

(a) Farm credit to individual farmers [including Self Help Groups (SHGs) or Joint

Liability Groups (JLGs),

(b) Farm credit to corporate farmers, FPOs/FPCs, Companies of Individual farmers, Partnership firms and cooperative farmers engaged in agriculture and allied activities),

(c) Agricultural Infrastructure

(d) Ancillary Services- Loans for Food and Agro-processing, loans to startups (as per the Ministry of Commerce and Industry regulations), deposits under RIDF, Loans by cooperatives to farmers for purchasing for purchase of the agricultural produce.

(e) Small and marginal farmers- for loans the category is broadened to include Farmers with landholding of up to 1 hectare (Marginal Farmers), Farmers with a landholding of more than 1 hectare and up to 2 hectares (Small Farmers), Landless agricultural labourers, tenant farmers, oral lessees and sharecroppers whose share of landholding is within the limits prescribed for SMFs, Loans to Self Help Groups (SHGs) or Joint Liability Groups (JLGs), i.e. groups of individual SMFs directly engaged in Agriculture and Allied Activities, provided banks maintain disaggregated data of such loans, loans to individuals solely engaged in allied activities without any accompanying land holding criteria etc.

(f) Lending by banks to MBFCs and MFIs for on-lending to agriculture.

- Micro, Small and Medium Enterprises 7.5 per cent – Factoring Transactions, Khadi and Village Industries Sector (KVI) and Other Finance to MSMEs.

- Export Credit: for foreign banks, incremental export credit norm for domestic banks, SFBs and UCBs (not applicable for RRBs and LABs).

- Education: Loans to individuals for educational purposes including vocational courses up to Rs 20 lakh.

- Housing: Loans to individuals up to Rs 35 lakh in metropolitan centers and loans up to Rs 25 lakh in other centers for purchase/construction of a dwelling unit per family.

- Social Infrastructure: Up to Rs 5 crores per borrower for building social infrastructure in schools, health care facilities, drinking water facilities and sanitation facilities. Bank loans to MFIs for on-lending to social infrastructure will also be eligible.

- Renewable Energy: Bank loans up to a limit of Rs 30 crores to borrowers (individual households- Rs 10 lakh).

- Others: SHG, JLG etc.

| Timeline for UCBs to achieve the PSL target of 75% | ||||

| March 31, 2020 | March 31, 2021 | March 31, 2022 | March 31, 2023 | March 31, 2024 |

| 40% | 45% | 50% | 60% | 75% |

Weaker Sections

From the above categories, a subcategory called Weaker Sections is also identified so that they can get special preference under PSL. The new regulations stipulate that banks should give 10% (2021 and be increased to 12% by 2024) of their loans to the weaker sections.

Weaker sections under the PSL

- Small and Marginal Farmers.

- Artisans, village and cottage industries where individual credit limits do not exceed Rs. 1 lakh.

- Beneficiaries under Government Sponsored Schemes such as National Rural Livelihoods Mission (NRLM), National Urban Livelihood Mission (NULM) and Self Employment Scheme for Rehabilitation of Manual Scavengers (SRMS).

- Scheduled Castes and Scheduled Tribes.

- Beneficiaries of Differential Rate of Interest (DRI) scheme.

- Self Help Groups.

- Distressed farmers indebted to non-institutional lenders.

- Distressed persons other than farmers.

- Individual women beneficiaries up to Rs. 1 lakh per borrower.

- Persons with disabilities.

- Minority communities may be notified by the Government of India from time to time.

Shortfall in PSL and the remedial measures: Banks (SCBs) having shortfall in lending to priority sector/subsectors vis-a-vis the stipulated targets are required to contribute to the funds of Rural Infrastructure Development Fund (RIDF) and similar funds set up with the National Bank of Agriculture and Rural Development (NABARD)/Small Industries Development Bank of India (SIDBI) / National Housing Bank (NHB).

Priority sector lending by SFBs and RRBs: Besides commercial banks, RRBs and Small Finance Banks are also providing PSL. The SFBs and RRBs are having a priority sector target of 75% of their adjusted net bank credit. The SFBs must serve their dedicated geographical locations regarding PSL. SFBs also issued priority sector lending certificates.

*********

?")